Credit Repair Alternative: Credit Report Education & Action Plan

If you knew that you could improve your financial health today, would you?

Credit scores are one vital component of your financial health, and raising your credit score unlocks a world of opportunity. Unfortunately, it takes time, but there are things you can do today that will pay off down the line.

Don’t put it off until tomorrow!

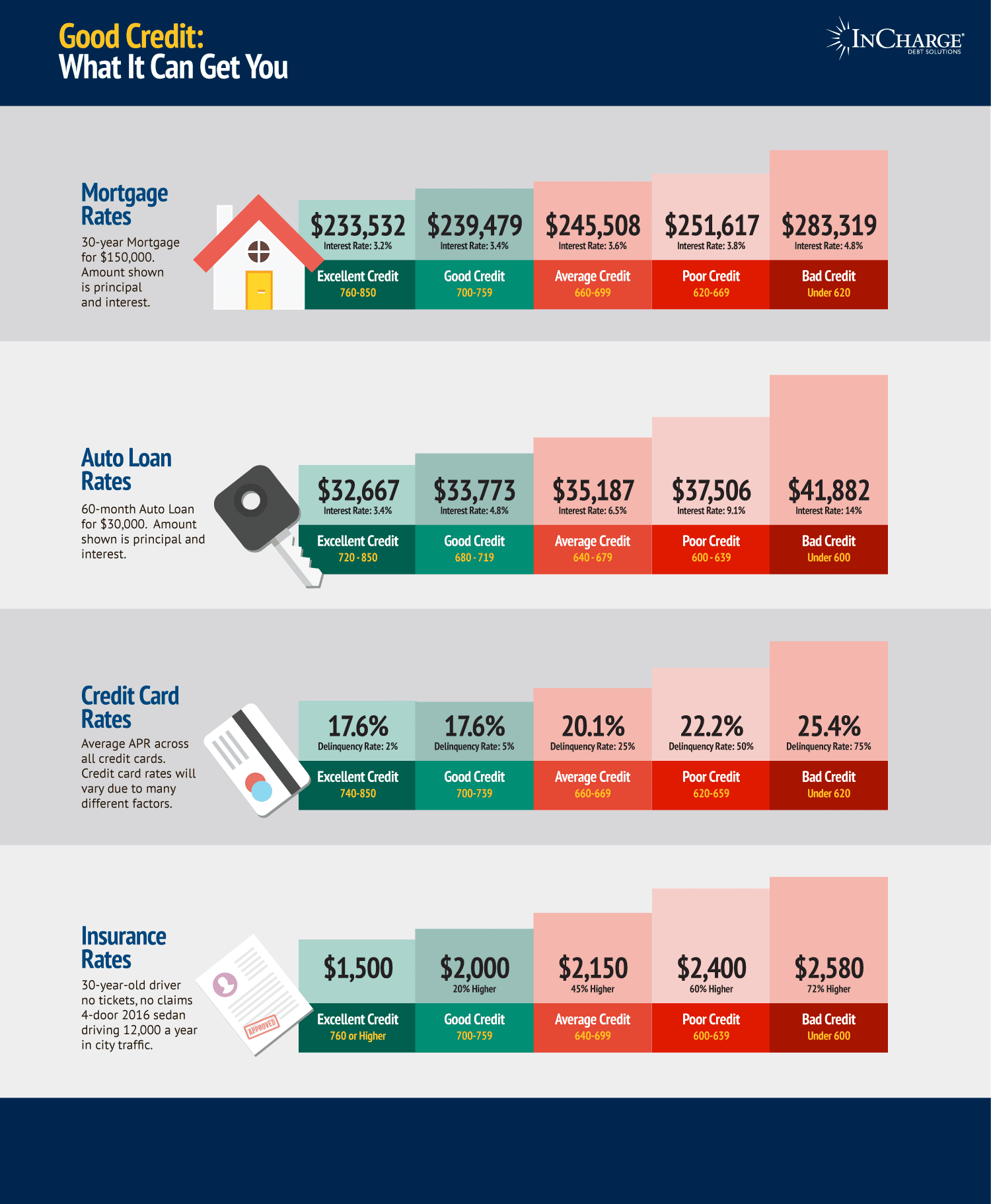

Lenders use credit scores to judge your trustworthiness in repaying a debt. Increasing your credit score to something north of 700 means you qualify for lower interest rates and favorable terms on any borrowing you do. Push the score above 750 and you should qualify for the best rates a lender offers.

Low credit scores have the opposite effect. You may not qualify for a loan to buy a car, a home or get insurance needed for either one. In fact, you can be denied housing, utilities and pay outrageously high interest rates on credit cards, if you have a bad credit score.

So, a good credit score – preferably 700 or higher – matters. Here are some steps you can take today that will get you there.

![]()

Seven Steps to Improve Your Credit Score

The fastest way to improve your credit score is to stop using your credit cards and pay down the balance on each and every one. Nothing beats making on-time payments every month, except maybe making them twice-a-month.

Don’t be afraid to devote some portion of every paycheck to reducing the balance on all debts, especially credit cards.

If you can get the balance on each card down to less than 30% of the available limit (e.g. under $300 on a credit card with a $1,000 credit limit), your credit score will start moving up. If you can get the balance down to zero, your credit score will jump up.

Here are some other steps that can improve your credit score:

1. Pay Your Bills on Time

If you’ve missed payments, catch up. If need be, set up automated reminders when payments are due. Or better yet, set up automatic payments from your bank account. Paying on time every month is the most crucial aspect of improving your credit score and easiest to control. Card companies reward consumers who are reliable with payments and punish those who don’t.

2. Don’t Close Old Accounts

Do not close the account on cards you no longer use. It will have a negative impact on credit utilization rate and average age of your accounts, two major factors in determining your credit score.

Keep the accounts open but keep paying on them so the balance goes down. The only reason to cancel a card is if there is an annual fee or some other transaction fee that is adding to your debt.

3. Monitor Credit for Errors

Monitor your credit report to make sure there are no inaccuracies that could reduce your score. Errors can send false signals to lenders that you are unreliable with credit, when in fact, the negative marks were no fault of your own. To check for errors, you can request an annual credit report from annualcreditreport.com. Each of the three credit reporting bureaus, Experian, Equifax and TransUnion, must furnish you a free credit report every year.

Monitoring your credit report may also alert you to identity theft if you see charges that don’t belong. Be sure to dispute a debt with creditors, bill collectors and reporting agencies if they are in error.

4. Limit Credit Applications

Do not apply for another credit card unless you really need one. Don’t pay off one credit card with another card. Opening multiple accounts in a short period of time is also a negative.

5. Work Out Payment Agreements

If you have overdue bills, bargain with the creditor to see if they will accept partial payments. If they do, have the creditor report the account as “paid as agreed.”

6. Ask for a Higher Credit Limit

Call your credit card company and request a higher spending limit. This will lower your credit utilization and make it easier to stay under the 30% spending recommended for card users. Ask the card issuer to do a “soft pull” on your credit report to make this happen. If you have been a steady payer, this should be an easy way to improve your credit score.

7. Get Professional Help

If you’d like to take these steps but don’t see how you can swing it, call a nonprofit credit counseling agency and ask for help coming up with a viable repayment plan such as a debt management program.

Credit Booster: Helping You Enhance Your Credit & Manage Your Debt – eBook

This book provides practical tips on how you can improve your credit score and credit report through improving your history of on-time payments, disputing incorrect information, reducing your credit utilization and maintaining a legacy credit card. Put these tips into practice today and watch your credit score improve.

Negative Factors in Your Credit Score

If you are in a hurry to improve your credit score, it is wise to understand the negative influences on your credit report and how long those negatives will be there.

Most negative influences on your credit report stay there for seven years, though their impact on your credit score goes down over time. In other words, it counts less in the fifth, sixth and seventh year than it did the first three.

The most obvious negative influence on a credit score is late payments, especially those that go to a bill collection agency, which can include evictions. A lesser known, but equally negative influence is found in debts listed in public records like bankruptcy and tax liens. Chapter 13 bankruptcy is on your report for seven years. A Chapter 7 bankruptcy is there for 10 years.

Tax liens are a slightly different story. They can stay on your credit report for seven years after they have been paid. However, the IRS will allow consumers who pay their tax liens to request they be removed from the credit reports immediately.

Why Your FICO Score Matters

FICO, or Fair Isaac Corporation, is the nation’s oldest and most trusted provider of credit scores. Over 90% of businesses use the FICO score to help determine a consumer’s creditworthiness.

FICO scores are the three digits that tell lenders how likely you are to pay back the loan on time. Unlike your weight or age, the higher the number, the happier you’ll be.

A score of 800-850 is considered excellent; 740-799 is very good; 670-739 is good; 580-669 is fair and anything below 580 is poor.

You can increase your score using the steps shown above, but they are not necessarily easy. If that prospect bothers you, blame William Fair and Earl Isaac, the founders of the credit scoring system. They were the mathematical engineers who devised the first credit-monitoring system in 1956.

Fair, Isaac and Company was eventually shortened to FICO, and it is the go-to information source for the three major credit-reporting agencies: Equifax, Experian and TransUnion. The three agencies’ evaluation methods differ slightly, but the final numbers consistently reflect your credit-worthiness.

The final numbers are all based on algorithms only pointy-headed professors like Fair and Isaac would truly comprehend, but here’s all you really need to know: Your age, race, religion, sex, marital status, address, income and employment history have no bearing.

Lenders will factor some of those in when deciding whether to give you a loan and other scoring systems may use that info, especially income and employment history, to calculate their scores, but FICO’s algorithms don’t care.

Only credit-related matters are considered. Your credit card history, mortgages and public records like bankruptcies, foreclosures, wage attachments and liens. Their importance diminishes over time, but bankruptcies stay on your score for 7-10 years.

How Is Your Credit Score Calculated?

FICO bases scores on five categories with varying percentages of importance:

Payment History – 35%

Payment history accounts for thirty-five percent of your score. Did you pay your credit account on time? Having no late payments doesn’t mean you’ll get a perfect score, however, since 60-65 percent of credit reports show no late payments, that would be considered a very good thing.

Amounts Owed – 30 %

That includes the total figure you owe and what percentage of your credit limit you use. For instance, if you have $7,200 on a Visa card with a $10,000 limit, your “credit utilization” is 72%. Experts suggest you limit credit utilization to under 30%, which in this case would be $3,000.

Having high balances shows you might be overextended. Some people believe they have to carry a balance to build credit. This is a myth. Paying a debt off early will help your credit score. Carrying a balance will hurt it.

Length of Credit History – 15 %

The longer you’ve used credit, the better. That’s why closing a long-standing credit account can hurt your credit score. The credit bureaus smile when they see someone has reliably used credit for a long time.

Credit Mix – 10 %

The combination of credit cards, installment loans, mortgages and other credit payments. As long as you make on-time payments, the more types of credit you have, the better.

New Credit – 10 %

Everybody has to start somewhere but opening several new credit accounts in a short period is a red flag. In other words, don’t apply for more than one or two credit cards at a time and make sure you keep your oldest credit cards open even when you get new ones. The average length of time you have had your credit cards matters.

Consolidate Debt With Bad Credit

Yes, you can consolidate your debt payments with bad credit by pursuing a debt consolidation alternative like a nonprofit debt management program.

More about bad credit

- How To Dispute A Mistake On My Credit Report?

- Will Multiple Credit Inquiries Hurt My Score?

- Does Paying A Loan Off Early Help Your Credit Score?

Why You Need Good Credit

Good credit will save you money by lowering interest rates when you want a mortgage or car loan, but it could also help you land a job or apartment.

More about why you need good credit

- Will My Credit Score Be Damaged If I Close Several Credit Card Accounts At Once?

- Fair Credit Reporting Act: Common Violations and Your Rights

- Credit Building Loans: What Are They, How to Get One and Do They Work

How Will A Short-Sale Affect My Credit Score?

After a short sale, what kind of hit can I expect on my credit score, and about what would be the recovery time for my credit score?

More about what can affect your credit score

Sources:

- ND. What’s in my FICO Scores. Retrieved from http://www.myfico.com/crediteducation/whatsinyourscore.aspx

- Arnold, C. (2014, May 2) 11 Ways to Raise Your Credit Score, Fast. Retrived from http://www.forbes.com/sites/moneybuilder/2014/05/02/11-ways-to-raise-your-credit-score-fast/#41d9aaf71716583a87f61716

- O’Connell, B. (2015, Aug. 21). Average U.S. Consumer Credit Score Is 695 – Here Are 5 Ways To Get Yours Above 800. Retrieved from http://money.usnews.com/money/personal-finance/articles/2015/06/23/10-simple-ways-to-raise-your-credit-score